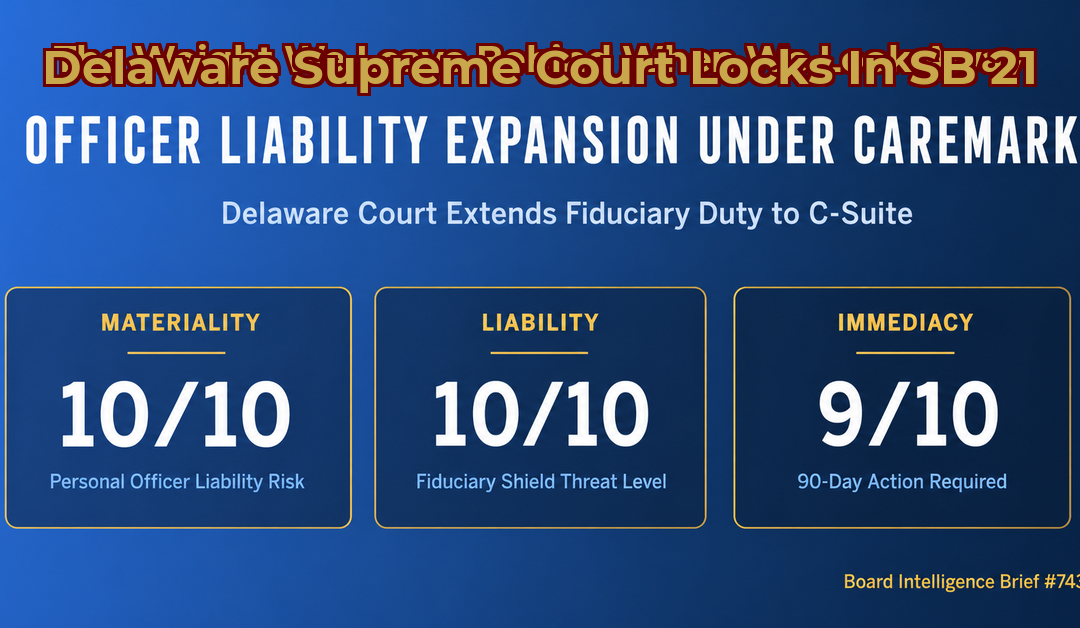

Executive Summary

The Delaware Supreme Court has unanimously upheld Senate Bill 21’s fiduciary safe harbors and retroactivity clause, clearing every constitutional challenge and remanding all pending conflicted-controller cases to the Court of Chancery for decision under the new, more management-friendly standard. Every Fortune 500 board with a controlling stockholder now operates under a materially different litigation calculus: minority stockholder suits that would have survived dismissal under prior Chancery doctrine may now be extinguished at the pleading stage. Boards that have not assessed their pending exposure and restructured any affiliate transactions accordingly should do so before the summer proxy season closes.

The Signal at a Glance

PRIORITY 10 | SILO: Judicial (Delaware Supreme Court)

The Delaware Supreme Court confirmed SB 21’s safe harbors are constitutionally valid, retroactively reshaping the fiduciary litigation standard for every controlling-stockholder transaction filed after February 17, 2025.

The Deep Dive

The Signal

On April 29, 2026, the Delaware Supreme Court issued a unanimous opinion in Rutledge v. Clearway Energy Group, Appeal No. 248, 2025, written by Justice Traynor. The court answered two certified constitutional questions and upheld both the safe harbor provisions and the retroactivity clause of Senate Bill 21 (SB 21), the March 2025 overhaul of the Delaware General Corporation Law (DGCL).

The decision ends the constitutional uncertainty that had placed SB 21’s reach in question across dozens of pending Chancery cases. The case now returns to the Court of Chancery, where the controller-defendant will move to dismiss on safe harbor grounds.

The Evidence

SB 21 was enacted in March 2025 in direct response to a wave of plaintiff-friendly Chancery decisions that had prompted several Delaware-domiciled companies to consider reincorporating in Texas or Nevada (the “DExit” threat). The legislation narrowed the definition of a controlling stockholder and created statutory cleansing mechanisms. For transactions that do not cash out minority stockholders, a single cleansing mechanism (either an independent committee or a disinterested stockholder vote) is now sufficient to insulate a transaction from judicial scrutiny, replacing the prior requirement for both.

The stockholder-plaintiff in Rutledge raised two constitutional objections. First, that SB 21 impermissibly limited the Court of Chancery’s equitable jurisdiction, which the Delaware Constitution protects. Second, that retroactive application deprived him of a vested right under Delaware’s Bill of Rights. The Supreme Court rejected both. It found that SB 21 modifies the standards of fiduciary conduct: how violations are measured and what remedies are available, without altering the Chancery Court’s jurisdiction to decide cases. On retroactivity, the court held that statutory changes to the rules of decision do not deprive plaintiffs of vested rights when those changes are incidental to a legitimate legislative policy.

The Strategic Implication

Defensive Risk. Every pending derivative suit challenging a controlling-stockholder transaction filed after February 17, 2025 now proceeds under a cleansing standard that is materially easier for management to satisfy. Boards facing such suits should reassess their litigation posture immediately: cases that counsel assessed as likely to survive dismissal under pre-SB 21 doctrine may now be dismissible on a properly constituted independent committee alone. Audit committees and general counsel should request updated litigation risk registers before the next board meeting.

Offensive Advantage. Boards of Delaware-incorporated companies with controlling stockholders can now structure affiliate transactions (acquisitions, asset transfers, related-party contracts) with substantially reduced litigation risk, provided the independent committee is properly constituted under SB 21’s statutory requirements. This opens a window for strategic transactions that prior Chancery doctrine had effectively priced out of reach for companies with concentrated ownership.

Tone at the Top

The Delaware Supreme Court’s Rutledge decision is the most consequential corporate governance ruling of 2026: it converts a contested legislative bet into settled law and resets the fiduciary litigation environment for every Delaware-domiciled company with a controlling stockholder. The coming year will produce the doctrinal detail as Chancery applies the new standard, and boards that understand the shift before those decisions arrive will hold a structural advantage.